Last week, Governor Cuomo released the 2020-2021 Executive Budget outlining priorities for spending $178 billion while closing the $6.1 billion gap.

The FY2021 budget marks the last funding year of the 5-year statewide affordable housing plan, which promises to create or preserve 100,000 units of affordable housing and 6,000 supportive housing units. The $20 billion initiative is not subject to public reporting, so we have limited details on spending and production progress. The budget briefing book says, “The State is well on track toward meeting that mark, having already financed the new construction and preservation of more than 60,000 affordable units.”

Over 5 years, the $20 billion is broken down into “$3.5 billion in capital resources, $8.6 billion in State and Federal tax credits and other allocations, and $8 billion to support the operation of shelters, supportive housing units, and rental subsidies.” While most of the capital funding for the affordable housing plan was appropriated in the first year of the plan, $407.336 million of the original funding is scheduled to be available starting April 1, 2020. In addition, the Executive Budget doubles funding for the Homeless Housing Assistance Program this year to $128 million for supportive housing operated by the Office of Temporary and Disability Assistance (OTDA). This includes $5 million dedicated to housing permanent, emergency and transitional housing for persons living with HIV or AIDS and another $5 million for veteran housing. With a record high statewide homeless count of 91,897, this additional funding is needed but more must also be done by the state to address our homeless crisis. The Executive Budget fails to include Home Stability Support funding which would prevent families from becoming homeless. NYS must also continue funding for the successful ESSHI program in order to ensure a continuous pipeline of critically needed supportive housing.

Notably, public housing was left out of the Executive Budget again this year. With capital needs now projected to be $40 billion in NYC alone, NY State must do more to preserve public housing across the state.

We were also hoping that the new Source of Income Law enacted last year in the budget would receive enforcement funding this year but it was left out. Read more about the #EndIncomeBiasNY campaign in a recent Op Ed by our partners, Elaine Gross from Erase Racism and Lorraine Collins from Enterprise Community Partners, Inc, “Section 8 discrimination is a crime, now Cuomo must fund enforcement”.

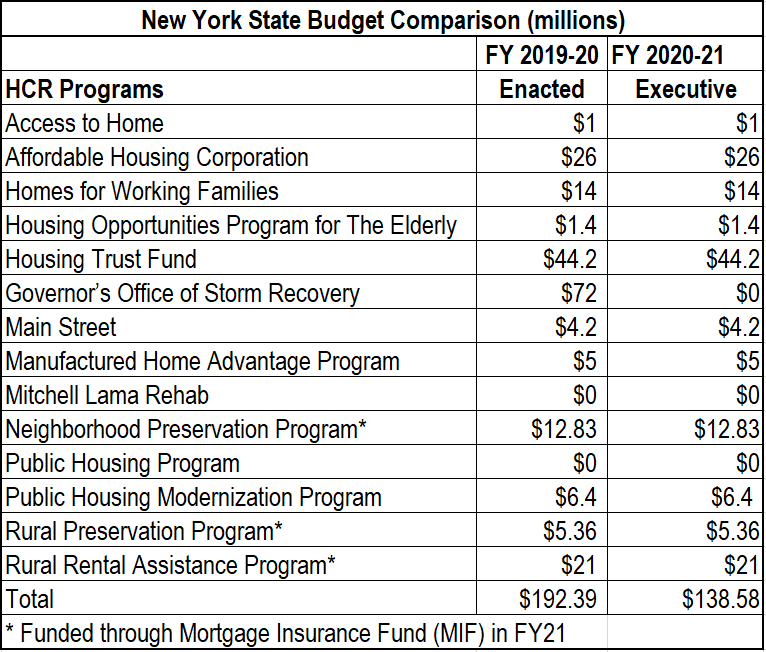

Additional capital proposed in the Executive Budget for HCR’s ongoing programs is detailed in the chart below.

Here are some other related policy and budget proposals:

- The Medicaid Redesign Team (MRT)

MRT is charged with identifying cost-containment measures that will provide approximately $2.5 billion in gap-closing savings in FY 2021 and ensure Medicaid spending in future years adheres to the Global Cap indexed rate. The spending targets are incorporated into the Financial Plan projections. The Team’s recommendations are due prior to the Enacted Budget on April 1 so there is not a lot of time to act. In the past, MRT had proposed investing in supportive and senior housing to reduce healthcare costs with great success. SKA Marin’s Metro East 99th Street is an example of how targeted investment in housing (in this case for chronically disabled individuals) can improve quality of life while saving tax dollars. We hope MRT will revive their housing committee as part of this process.

- New Authority to Reduce NYC Funding to Offset Costs Incurred for Administering Rent Regulation

NYC already pays NYS to administer rent regulation according the emergency tenant protection act of 1974, amended in 2019. HCR establishes an estimate and there is codified schedule of payment. This new amendment would allow the director of the budget to direct any other state agency to reduce the amount of any other payment or payments owed to such city or any department, agency, or instrumentality thereof; provided however, that such reduction shall be in an amount equal to the costs incurred by the state in administering the rent regulation program for such city.

- Abolish the State Board of Real Property Tax Services

This transfers remaining duties of this State Board to the Commissioner of Taxation and Finance. In 2010, when the responsibilities of the State Office of Real Property Services were transferred to the Department of Taxation and Finance, the State Board of Real Property Services was retained and renamed the State Board of Real Property Tax Services. This bill would abolish that board and thereby make the process of reviewing and determining complaints involving equalization rates, special franchise assessments, and certain assessment ceilings more efficient, while aligning the Department of Taxation and Finance with other agencies, and eliminating instances where complaints cannot be resolved due to the lack of a quorum.

- Provides a Local Option for Placing Converted Condos Into the Homestead Class Purpose

This proposal would give municipalities that have separate tax rates for homestead and non-homestead properties, and that value converted condos using the sales approach, the local option of placing converted condominiums in the homestead class.

- Deny STAR Benefits to Delinquent Property Owners

Provides state support for the local enforcement of past-due property taxes, by precluding delinquent property owners from receiving STAR credits or exemptions if their property taxes remain unpaid.

- Allow for the Appointment of Acting County Directors of Real Property Tax Services

Amends the Real Property Tax Law (RPTL) to allow for the appointment of an Acting Director of Real Property Tax Services in the event that the appointed Director of Real Property Tax Services is unable to perform the duties of the office or the office becomes vacant.

- Modernize and Merge Real Property Tax Forms and Processes

When real property is sold, two different State-prescribed forms must be filed, both on paper, and a real estate transfer tax (RETT) must be paid, unless an exemption from the tax applies. The two forms (TP-584 and RP-5217) are largely duplicative of one another, but they cannot be readily combined because one form is a RETT return that is subject to the secrecy provisions of the Tax Law, and the other is a real property tax report that, by law, is fully subject to public disclosure. This bill would authorize the Commissioner of Taxation and Finance to combine these two forms into a consolidated real property transfer form and to implement an online system for e-filing this consolidated form and paying the associated taxes and fees. In New York City and Westchester County, which have instituted their own electronic deed recording systems, the Department’s e-filing option would be available only if the city or county opted to allow it to be used.

- Make Exceptions for Late Enhanced STAR Filers

This bill would reopen the enrollment period for the STAR Income Verification Program (IVP) and allow DTF to send checks to qualified late enrollees.

- Shift Basic STAR Exemptions to the Credit Program

The bill would reduce the income limit for the Basic STAR exemption from $250,000 to $200,000. Property owners with incomes greater than $200,000 who had been receiving the Basic STAR exemption on the preceding assessment roll would be switched automatically to the Basic STAR credit, unless the Commissioner of Taxation and Finance is unable to verify their eligibility for the credit, in which case they will be notified and given an opportunity to demonstrate their eligibility.

For more information on this policy proposals, click here.